VC 2025: AI, Blockchain, and Everyone Entreperneurs

Venture capital looks very different in 2025: huge funds hold most of the cash, deal counts are down, AI gets nearly half of all new money, and solo founders can launch a product in a weekend. What does this tug-of-war mean for investors hunting returns and builders chasing their first dollar?

The article is laid out according to the following content:

- Fewer deals, fatter rounds – Deal count sinks, average check size soars.

- AI soaks up the cash – Nearly half of all U.S. VC dollars now target AI.

- Founders go lean – Gen-AI and no-code let one-person teams launch for < $100.

- Funding gaps widen – Tiny startups need micro-checks; mega-funds play late-stage.

- New models rise – Micro-VCs, revenue-based loans, and tokenized community rounds step in.

Section 1. VC 2025: Fewer Checks & Bigger Bets

VC Market in General

US venture funding has slipped into a “big-but-rare” phase: fewer deals close, but the cash behind each one swells—and it’s pooling inside a handful of megafunds.

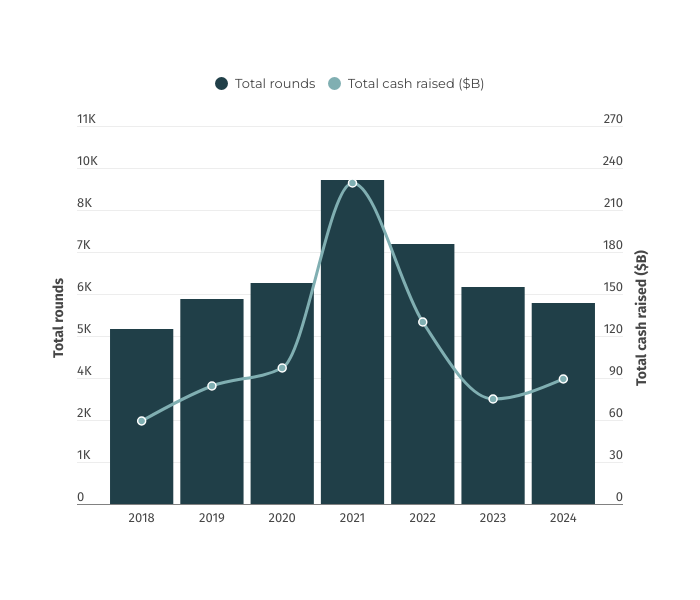

- Deals down, dollars up – Startups closed 5,743 equity rounds in 2024 (-7% YoY, lowest since 2018), yet total capital jumped 18 %, pushing the average round to $15.5 M (+28% YoY), according to Carta.

- Megafunds dominate – New-fund launches fell 46 % YoY (-68% vs 2021), but the average fund size ballooned 44%. Just nine marquee firms captured around 50% of all U.S. VC commitments.

And the rest of the world is marching the same way: global VC deal count slid 19% YoY to around 27 k (lowest since 2016), yet only 463 $100 M+ mega-rounds soaked up $135 B – nearly half of 2024’s $275 B worldwide funding pool.

AI Dominance

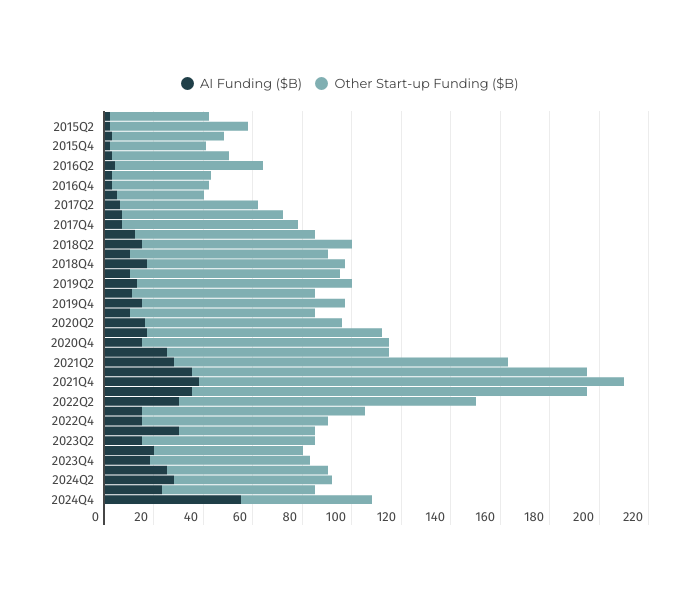

PitchBook counts $97 billion poured into U.S. AI startups in 2024 – 46 % of all domestic VC deployment. Globally, Crunchbase estimates AI deals hit $100 billion, up 80 % YoY. Because modern AI companies can launch with smaller teams and heavy cloud credits, they consume less capital per milestone, threatening the “spray-and-pray” model that relied on big check sizes to drive management fees.

Web3 Fade

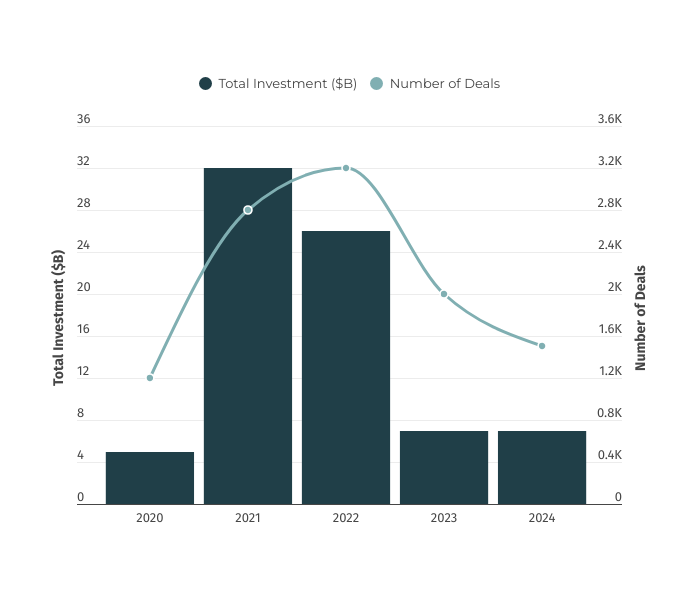

After a $30 billion peak in 2021, VC funding to blockchain/Web3 startups slid to just $8.5 billion across 1,545 deals in 2024 – barely 3 % of global venture dollars and down 26 % in deal volume from the prior year, according to Crunchbase. Even modest quarterly rebounds haven’t reversed the longer-term slump as investor attention (and LP patience) shifts to AI.

Section 2. The Era of Everyone Entrepreneurs

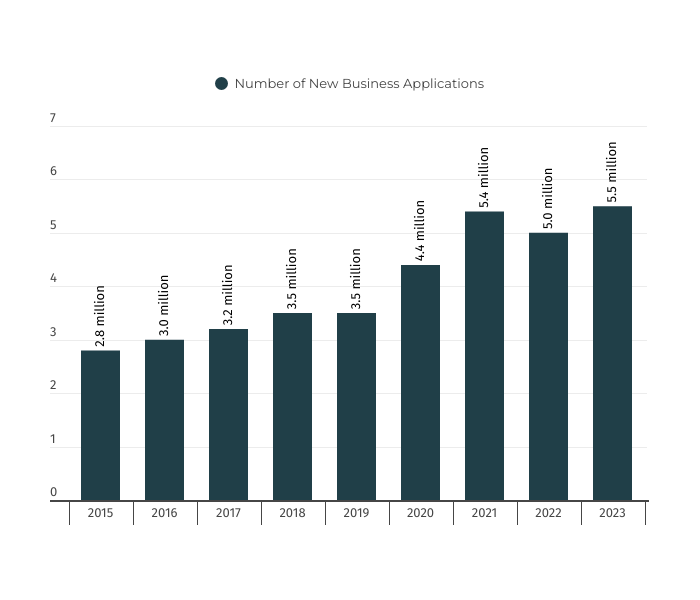

New data from the U.S. Census Bureau show just how quickly entrepreneurship is spreading: Americans filed 5.5 million new business applications in 2023 – almost twice as many as in 2015 and the third year in a row above the five-million mark, according to Commerce Institute. Early 2025 figures suggest the pace is still well above pre-pandemic levels.

What’s driving this boom?

- Generative AI – now drafts code, marketing copy, slide decks, and even customer-support emails. A motivated founder can spin up a polished product and brand over a single weekend for well under $100 in cloud credits and API fees.

- No-code and low-code tools – (think Bubble, Webflow, Glide, Notion apps) let non-technical builders launch real software with simple drag-and-drop interfaces. Basic plans start around $30 a month, eliminating the need for a hired dev team.

- Blockchain rails – (likely) give small startups instant global payments and new ways to raise funds—from token-based community rounds to on-chain revenue sharing—at only a few dollars in gas fees.

What does this mean for the startup landscape?

- Micro-startups and solo founders are multiplying – A single person can now ship an MVP, acquire first customers, and reach profitability on a shoestring.

- Capital efficiency is the new default – When you can build for hundreds—not millions—of dollars, the traditional VC playbook of outsized seed rounds and blitz-scaling makes little sense for most founders.

- Long-tail innovation is exploding – Niche, under-served problems (local, vertical, creator-focused) that were uneconomic for large teams are suddenly viable businesses.

- Funding models must adapt – These lean ventures need micro-checks, revenue-based financing, token crowdsales, or community syndicates—not $10 million Series A rounds geared for 100× exits.

Section 3. VC vs Founders: The Mismatch

Emerging technologies like AI and blockchain have dramatically reduced the barriers to entrepreneurship, enabling millions of capital-efficient founders to launch ventures with minimal resources, yet the venture capital landscape remains misaligned, with most funds focused on large, later-stage investments, as shown in the current market trend.

| Market reality | Traditional VC model | Resulting gap |

|---|---|---|

| Millions of lean founders need tiny amounts of flexible capital. | Funds are larger, later-stage, and optimized for $10 m-$50 m checks. | Early-stage and micro-funding dries up; founders turn to alt-financing. |

Section 4. Alternative VC Models

Traditional VC bundles three things—money, governance, and hands-on help – into one large (and often late-stage) check. Today that bundle is being unpacked. A fast-growing mix of smaller, more specialized funding models now let founders pick only the piece they need – and pay with something other than big chunks of equity. The models are listed here:

- Micro-VCs – Micro-VCs are sub-$100 million funds—often led by former startup operators—that write quick $250 k–$2 m seed checks in tightly defined niches. They move fast and offer hard-won operator advice, but their small size leaves little capital for later follow-on rounds.

- Revenue-Based Financing (RBF) – RBF gives founders an upfront lump sum, repaid as 5–20 % of monthly revenue until a fixed cap is hit, so payments scale with sales. It delivers dilution-free cash in days, yet if growth slows the repayment burden still sits squarely on the company.

- Equity Crowdfunding (ECF) – ECF platforms let thousands of retail investors buy small equity stakes under JOBS Act rules, turning loyal customers into shareholders. The campaign doubles as marketing and social proof, but lighter diligence and illiquid shares can make later VCs wary.

- Venture DAOs – Venture DAOs are token-based, community-run funds where members vote on deals via smart contracts, enabling borderless capital and collective expertise. Transparency is high, though whale dominance, governance gridlock, and murky legal protections remain real risks.

| Feature | Traditional | Micro-VC | RBF | ECF | Venture DAO |

|---|---|---|---|---|---|

| Typical Check Size | $5M - $50M+ | $100k - $2M | $50k - $5M | $100k - $5M (aggregated) | Varies widely |

| Target Stage | Series A and beyond | Pre-Seed, Seed | Post-Revenue, Growth | Pre-Seed, Seed | Pre-Seed, Seed (often Web3) |

| Founder Control | Low (Board Seat, Veto Rights) | Medium (Advisory, less formal) | High (Full control) | High (No direct investor control) | Low (Decentralized governance) |

| Ideal Candidate | High-growth, power-law potential | Niche, deep-tech, founder needing expertise | SaaS, E-commerce with recurring revenue | B2C, strong brand story | Web3, decentralized protocols |

| Value-Add | Network, Governance, Scaling | Specialized Coaching, Niche Network | Purely Capital, Financial Flexibility | Market Validation, Brand Advocates | Decentralized Community, Web3 Network |

Section 5. Future

A fragmented funding landscape doesn’t spell the end of venture capital—it’s forcing it to upgrade. Savvy VC firms now re-bundle tools like scout checks, revenue loans, and DAOs into one seamless platform, letting them stay active in seed rounds and own the later stages too.

The Decentralized Edge: Scout Programs and Founder-Led Funds

- Top VCs now arm trusted founders, operators, and domain experts with $50k–$100k “scout” checks. These tiny tickets cost the firm almost nothing, yet broadcast a dense web of sensors into communities that traditional partners rarely reach. The payoff is a proprietary, early look at high-potential teams long before a formal seed round.

Key highlight: Always-on, low-cost deal-radar that feeds the main fund’s Series A pipeline.

The Quant VC: Integrating AI into the Investment Lifecycle

- Algorithms now scrape hiring data, patent filings, and social momentum to flag hidden startups, then auto-check financial models and contracts during diligence. Post-investment dashboards monitor web traffic, sentiment, and churn in real time. Human intuition still calls the shots—but it’s now supercharged by always-updating data feeds.

Key highlight: Faster, broader, and more objective decisions across sourcing, diligence, and portfolio monitoring.

The Specialist Play: The Rise of Sector-Focused and Dedicated Seed Funds

- Mega-firms are spinning up deep-domain funds (biotech, fintech, climate) and nine-figure seed vehicles that mimic micro-VC intimacy while supplying big-firm firepower. Sector focus builds credibility with niche founders; large reserves ensure follow-on capacity that small funds can’t match.

Key highlight: Combines micro-VC hands-on support with the brand, network, and check size of a global platform.

Section 6. For Founders and Investors

Venture capital is being rebuilt in real time. Cash is piling into a few mega-funds, yet the real action is at the edges where one-person startups, micro-checks, revenue shares, and token crowds form a modular funding stack. Established firms are racing to stitch those modules back together with AI, scout networks, and sector seed vehicles, while community-run pools experiment with an open, borderless alternative.

What to watch:

- Which architecture wins? Will AI-powered mega-platforms consolidate the stack, or will decentralized, community funds out-innovate them?

- Can capital stay truly modular? As founders mix and match micro-VC, RBF, crowdfunding, and DAOs, will any one model dominate, or will a permanent menu replace the old prix-fixe?

- Who keeps the edge? When anyone can launch a product for $100, what new advantages will investors—and founders—need to create outsized returns?

The answers will decide whether the next decade of venture belongs to concentrated giants, collaborative networks, or something we haven’t imagined yet.

About Global Venturing Labs (GVL)

We warmly welcome you to join our collaborative tech-driven venturing ecosystem.

GVL is a tech-driven venturing platform that empowers innovators by harnessing next-generation technologies, with a focus on AI and blockchain, to fund innovative ideas and drive wealth creation. GVL fosters an ecosystem where founders, investors, tech experts, and visionaries collaborate seamlessly, transforming concepts into reality in a new era of decentralized venture creation.

Mission and Pillars

- Co-Knowledge Base – Delivering actionable insights, tools, and real-world examples to guide innovators in building thriving ventures. We empower our partners to share their expertise, fostering collective growth and innovation.

- Co-Community Networks – Fostering a global network of visionaries-founders, tech experts, investors, and enthusiasts – to connect, collaborate, and drive innovation.

- Co-Venture Platform – A future decentralized, DAO-based platform empowering members to launch businesses and invest through community-driven funding. We aim to provide values beyond capital.

Join us for the next-gen collaborative venturing!