Stablecoins: A Fundamental Guide

The future of money is here, powered by a technology already moving billions in value daily: the stablecoin.

Stablecoins combine the stability of traditional currencies, like the U.S. dollar, with the speed and global reach of the internet. As landmark regulations like the GENIUS Act provide clarity, these digital assets are transforming from a niche tool into the foundational layer for the next generation of global commerce. This guide explains everything you need to know:

- Stablecoins are…

- History

- Categories

- Comparison: Stablecoins vs. Crypto & CBDCs

- Market

- Regulation

- Institutions

- For Founders & Investors

- Reports Collectionz

Section 1. Fundamentals

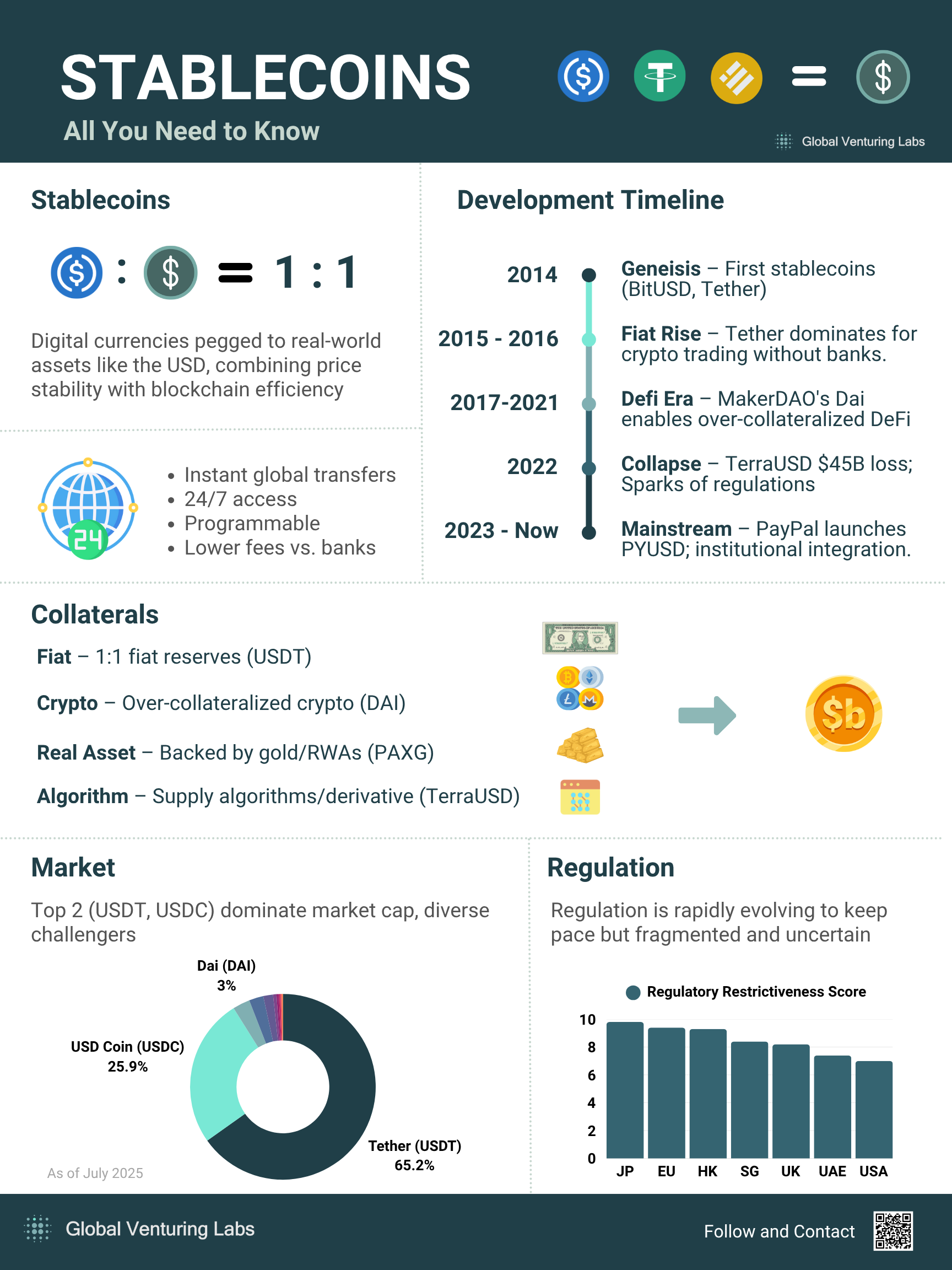

Imagine a digital dollar that moves at the speed of the internet but holds the steady value of the cash in your bank. That is the essential promise of a stablecoin. It is a type of cryptocurrency specifically engineered for price stability, typically by being pegged one-to-one with a real-world asset like the U.S. dollar. This makes it the indispensable bridge between traditional finance and the on-chain world, combining the security of established currency with the powerful advantages of blockchain technology. These benefits include:

- Combines the Real and On-Chain Worlds: Offers the trust and stability of traditional currency with the modern benefits of blockchain technology.

- 24/7 Global Access: Transactions can be sent anywhere in the world at any time, without relying on traditional banking hours.

- Near-Instant Settlement & Lower Costs: Enables fast, low-cost transactions with near-instant settlement by reducing the need for intermediaries.

- Programmable Payments & Automation: Can be integrated directly into smart contracts to create and automate complex financial services and transactions.

Section 2. History

- 2014: Genesis & Early Failures The first stablecoins emerged, including crypto-collateralized BitUSD and the fiat-backed model that became Tether. Early decentralized versions quickly failed due to unstable collateral, teaching the market a crucial lesson.

- 2014–2017: The Rise of Fiat-Backing In the wake of early failures, Tether’s simpler, fiat-backed model thrived. It became the essential stable asset for crypto traders to move between volatile positions without relying on the traditional banking system.

- 2017–2021: The DeFi Era & Decentralized Revival MakerDAO launched Dai, a more sophisticated decentralized stablecoin. Its key innovations, like significant over-collateralization, made it a foundational pillar for the growing Decentralized Finance (DeFi) ecosystem.

- 2022: The Algorithmic Collapse The catastrophic collapse of the algorithmic stablecoin TerraUSD (UST) wiped out over $45 billion in value. The event demonstrated the extreme risks of uncollateralized models and triggered intense global regulatory scrutiny.

- 2023–Present: Mainstream & Institutional Adoption The market matured beyond the shock, entering a phase of mainstream integration. Major companies like PayPal launched their own stablecoins, and retailers began accepting them for payments, signaling a shift toward real-world utility.

Section 3. Categories

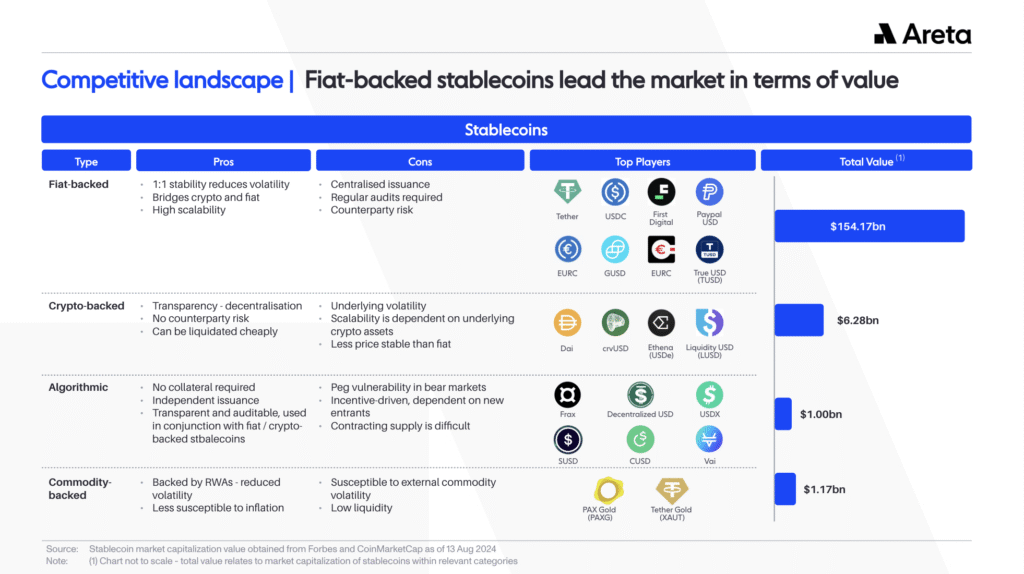

The value of a stablecoin is entirely dependent on the credibility of its pegging mechanism. The market has evolved through various models, each with unique risks and trade-offs, often learning from high-profile failures that exposed design vulnerabilities. Today, a few key architectures dominate the landscape, with fiat-collateralized stablecoins representing the vast majority of circulating value. The four primary models for achieving stability are:

- Fiat-Collateralized: Backed on a one-to-one basis by reserves of a specific fiat currency or cash equivalents held in custody.

- Crypto-Collateralized: Secured by an over-collateralized pool of other crypto assets managed entirely by on-chain smart contracts.

- Algorithmic & Hybrid: Relies on algorithms to manage supply or combines collateral with complex financial strategies like derivatives to maintain a peg.

- Commodity & Asset-Backed: Backed by physical commodities like gold or other tokenized Real-World Assets (RWAs) like U.S. Treasury bills.

| Model Type | Mechanism | Primary Risk | Examples |

|---|---|---|---|

| Fiat-Collateralized | Backed 1:1 by fiat reserves held with a custodian. | Centralization: Requires trust in the issuer and custodian; reserve transparency is critical. | USDC, USDT, PYUSD |

| Crypto-Collateralized | Over-collateralized by crypto assets locked in a smart contract. | Technical: Smart contract bugs, oracle manipulation, and cascading liquidations. | Dai (DAI) |

| Algorithmic & Hybrid | Algorithms manage token supply; hybrids use derivative strategies. | Fragility: Prone to "death spirals" if market confidence is lost; complex market risks. | TerraUSD (UST, failed), Ethena (USDe) |

| Commodity & Asset-Backed | Backed by physical commodities or tokenized financial assets. | Custodial: Relies on a trusted third party to store and audit the underlying assets. | PAX Gold (PAXG), Ondo (OUSG) |

Section 4. Stablecoins vs. Cryptos and CBDCs

Stablecoins merge the stability of traditional currency with the programmable innovation of blockchain, setting them apart from both volatile cryptos and government-controlled Central Bank Digital Currencies (CBDCs).

| Feature | Stablecoins | Cryptos | CBDCs |

|---|---|---|---|

| Issuer | Private Company | Decentralized Network | Central Bank |

| Value & Stability | Stable; Pegged to Reserves | Volatile; Market-Driven | Stable; State-Guaranteed |

| Control & Purpose | Private Control; Programmable Commerce | Decentralized Control; Peer-to-Peer Transactions | Government Control; Monetary Policy |

| Primary Use | Payments, Trading, DeFi | Speculation, Savings | Retail Payments, Bank Settlements |

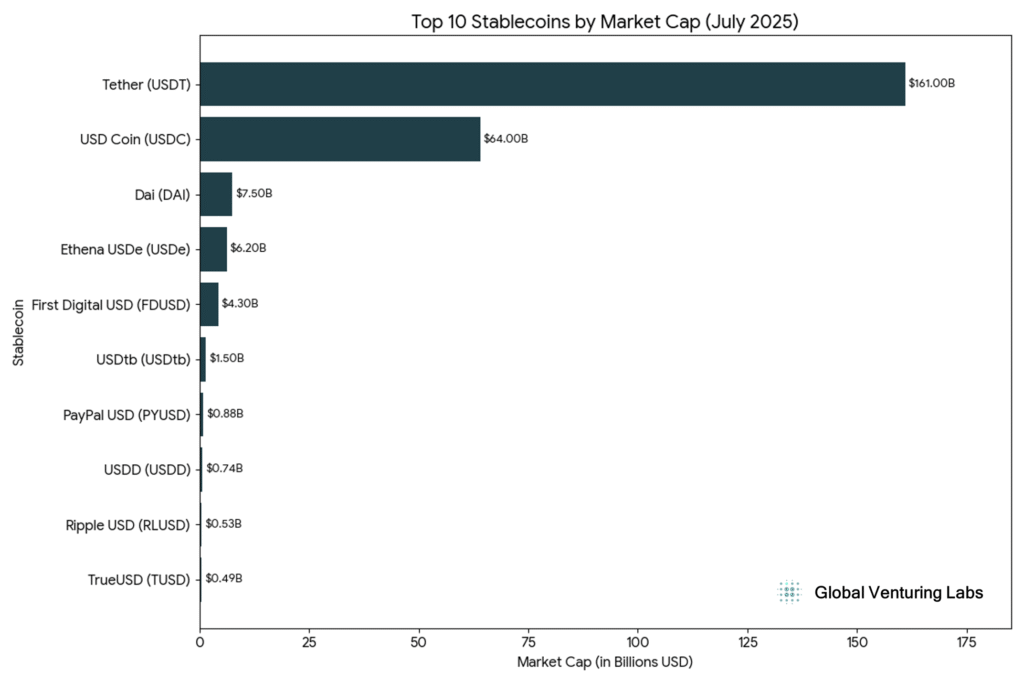

Section 5. Market

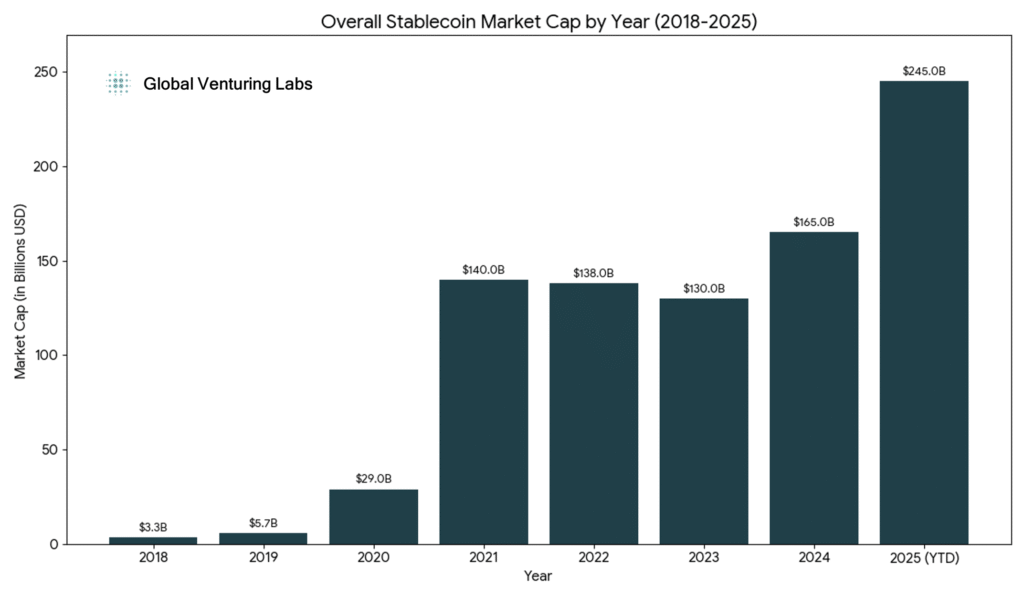

The stablecoin market is highly concentrated, with the top two assets commanding the vast majority of market capitalization and creating a significant gap to all other competitors. Below this dominant tier, the field becomes more diverse, featuring a mix of decentralized, crypto-collateralized models and newer synthetic dollar protocols that challenge the established, centralized leaders.

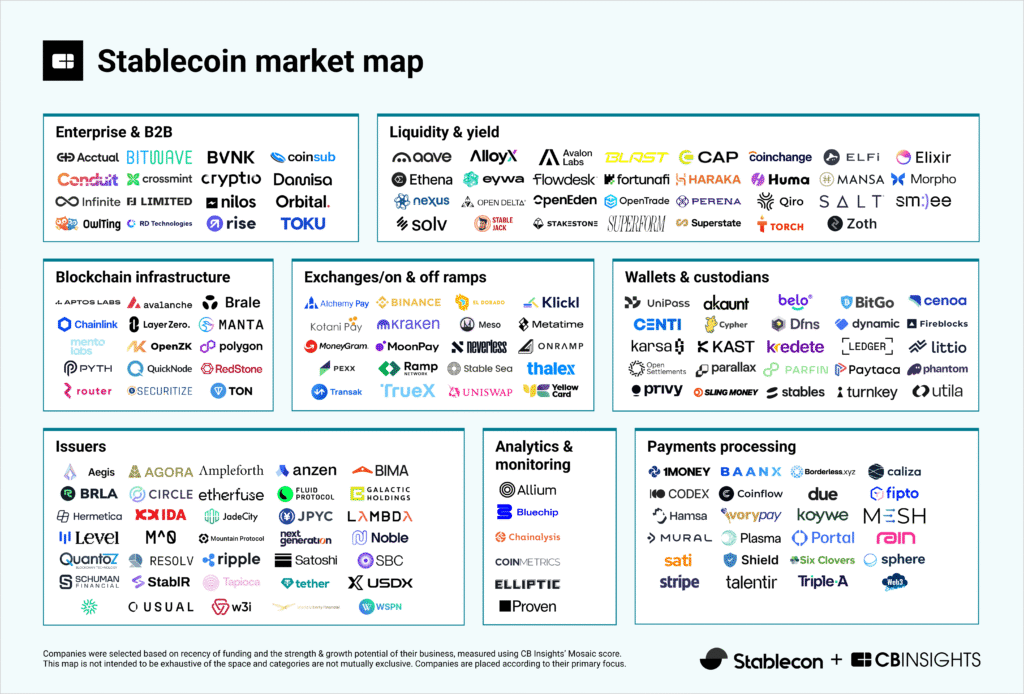

Beyond the issuers themselves, a rich ecosystem of infrastructure providers, payment processors, and analytics firms has emerged to support the stablecoin economy, as illustrated by the following market map.

Section 6. Regulations

Clear regulations are the starting gun for a profound transformation in finance. These new rules are the catalyst dissolving the boundaries between traditional institutions and the crypto-native world. Previously constrained by legal uncertainty, financial giants are now moving decisively to claim their stake in digital money. The table below outlines regulatory approaches across key global jurisdictions:

| Jurisdiction | Key Framework | Licensing Authority | Issuer Eligibility | Reserve Requirements | Evaluation |

|---|---|---|---|---|---|

| United States | GENIUS Act (Proposed) | OCC (Federal) / Certified States | Banks or licensed issuers; non-financial firms restricted. | 1:1 backing; cash or high-quality liquid assets (HQLA). | Pragmatic but Restrictive |

| European Union | MiCA | National Authorities / EBA | Licensed Credit Institution or Electronic Money Institution (EMI). | 1:1 backing; liquid reserves with 3rd-party custodian. | Comprehensive & Strict |

| United Kingdom | Financial Services & Markets Act (FSMA) | Financial Conduct Authority (FCA) | FCA-authorized firm. | 100% HQLA backing held in a statutory trust. | Strict |

| Hong Kong | Stablecoins Ordinance | HK Monetary Authority (HKMA) | Locally incorporated company; HK$25M min. capital. | 1:1 backing with HQLA; daily reconciliation. | Highly Restrictive / Exclusive |

| Singapore | MAS Stablecoin Framework | Monetary Authority of Singapore (MAS) | MAS-licensed entity; S$1M min. capital. | 100% backing; cash or short-term gov't bonds. | Restrictive & Prescriptive |

| Japan | Amended Payment Services Act | Financial Services Agency (FSA) | Licensed financial institutions only (banks, trusts, etc.). | Must be fully backed. | Highly Restrictive / Bank-Centric |

Section 7. Institutions Adoption

Global banks, the traditional custodians of money and trust, are now becoming issuers and infrastructure providers for digital currency.

- JPMorgan: Processes over $1 billion in daily wholesale payments with its permissioned, blockchain-based JPM Coin.

- BlackRock: Launched the BlackRock USD Institutional Digital Liquidity Fund (BUIDL), a tokenized money market fund whose shares are now used as a reserve asset by other stablecoins.

- Visa: Processes large-scale USDC stablecoin settlements and has launched a platform to help banks issue their own stablecoins.

- PayPal: Launched its own stablecoin, PYUSD, fully backed by U.S. dollar deposits, and is integrating it across its consumer payment network.

- Stripe: Enables its merchant customers to accept stablecoin payments and is building out its on-ramp and off-ramp infrastructure.

- Citi: Launched Citi Token Services to provide its corporate clients with 24/7, programmable cross-border fund transfers.

- Bank of America: Publicly confirmed extensive work on stablecoins and is reportedly in talks with other major US banks to develop a shared digital dollar.

- BBVA: Partnering with Visa to launch a stablecoin in 2025.

GVL Takeaways for Founders and Investors:

The stablecoin ecosystem is a greenfield for innovation. Opportunities exist across the entire technology stack, including:

- Global Payment Innovation: Regulated stablecoins offer superior back-end technology to disrupt the slow and expensive traditional payments industry. Founders can build “Payments-as-a-Service” platforms for cross-border B2B payments, remittances, and global payroll that are significantly faster (settling in minutes vs. days), cheaper, and more transparent than systems like SWIFT.

- Advanced Corporate Treasury Solutions: Stablecoins enable the creation of “Corporate Treasury-as-a-Service” platforms. These services allow businesses to manage global liquidity more efficiently in a single, 24/7 digital dollar pool, hedge against local currency inflation in volatile markets, and transform their treasury from a cost center into a profit center by accessing secure, on-chain yield opportunities.

- Real-World Asset (RWA) Tokenization: Perhaps the most transformative opportunity is building the foundational layers for the RWA market. Regulated stablecoins act as the essential on-chain settlement currency for tokenizing and trading trillions of dollars in traditionally illiquid assets like real estate, private credit, and government bonds, creating more efficient and accessible capital markets.

- Institutional DeFi and On-Chain Yield: For investors, regulated stablecoins serve as a trusted bridge to the Decentralized Finance (DeFi) ecosystem. This unlocks new investment opportunities, from venture capital bets on the “picks and shovels” (e.g., payment providers, compliance tools) to institutional strategies for generating yield by deploying stablecoins in audited lending protocols and RWA-backed products.

List of Reports

- International Monetary Fund (IMF): Decrypting Crypto: How to Estimate International Stablecoin Flows

- U.S. Federal Reserve: Primary and Secondary Markets for Stablecoins

- McKinsey & Company: The stable door opens: How tokenized cash enables next-gen payments

- Deloitte: The era of payment stablecoins has arrived

- World Bank: Crypto-Assets Activity around the World: Evolution and Macro-Financial Drivers

- Bank for International Settlements (BIS): Stablecoin growth – policy challenges and approaches

- Financial Stability Board (FSB): Regulation, supervision and oversight of global stablecoin arrangements: final report and high-level recommendations

- U.S. Department of the Treasury: Report on Stablecoins

About Global Venturing Labs (GVL)

We warmly welcome you to join our collaborative tech-driven venturing ecosystem.

GVL is a tech-driven venturing platform that empowers innovators by harnessing next-generation technologies, with a focus on AI and blockchain, to fund innovative ideas and drive wealth creation. GVL fosters an ecosystem where founders, investors, tech experts, and visionaries collaborate seamlessly, transforming concepts into reality in a new era of decentralized venture creation.

Mission and Pillars

- Co-Knowledge Base – Delivering actionable insights, tools, and real-world examples to guide innovators in building thriving ventures. We empower our partners to share their expertise, fostering collective growth and innovation.

- Co-Community Networks – Fostering a global network of visionaries-founders, tech experts, investors, and enthusiasts – to connect, collaborate, and drive innovation.

- Co-Venture Platform – A future decentralized, DAO-based platform empowering members to launch businesses and invest through community-driven funding. We aim to provide values beyond capital.

Join us for the next-gen collaborative venturing!