How Many Stablecoins Do We Need

Authors:

The Questions

- Why are the biggest names in finance and tech all racing to issue their own unique digital dollars?

- Could a flood of competing “corporate dollars” create a more fragmented and risky financial landscape?

- What will the future of money look like: a single dominant dollar, or a network of many that are seamlessly connected?

Section 1. Transition

The world of digital assets is going through a major change. Once created mainly by crypto startups, stablecoins are now attracting the world’s biggest financial and tech companies, including JPMorgan Chase and PayPal.

This strategic move is happening for two main factors: the arrival of long-awaited clearer government rules (like MiCA in Europe and the GENIUS Act in the U.S.) and the potential for digital tokens to unlock huge gains in efficiency. With legal barriers falling away, the time for exploring this technology is over, and the era of building real products has begun.

A wave of recent announcements confirms this trend. Major banks across the globe are revealing plans, from Citi and Bank of America in the U.S. to Kakao Bank in Asia and BBVA in Europe. They are being joined by digital wallet giant MetaMask and other major players like Amazon and Walmart. This rush of new players comes as the market is already dominated by established leaders like USDT and USDC. It raises three critical questions:

- Why are the biggest names in finance and tech all racing to issue their own unique digital dollars?

- Could a flood of competing “corporate dollars” create a more fragmented and risky financial landscape?

- What will the future of money look like: a single dominant dollar, or a network of many that are seamlessly connected?

Section 2. Definition and Market

Stablecoins are cryptocurrencies designed to maintain a stable value relative to a reference asset, typically a fiat currency like the U.S. dollar. They bridge traditional finance (TradFi) and the digital asset economy by combining the stability of government-issued money with the advantages of blockchain technology: speed, accessibility, transparency, and programmability. There are four main models of stablecoins, categorized by their underlying collateral:

- Fiat: This is the most trusted and institutionally accepted model, where each token is backed one-to-one by high-quality reserves like cash or short-term government securities. Examples include USDC. Issuers promise redemption at par, with trust relying on regularly audited reserves.

- Crypto: These are backed by volatile cryptocurrencies like Ethereum, requiring over-collateralization (e.g., $200 in Ether for a $100 stablecoin) to buffer against price swings. While this decentralized approach is suitable for DeFi, it is generally considered too risky for institutions.

- Real Asset: Pegged to real assets like gold, these stablecoins represent a claim on physical commodities held in vaults. They provide tokenized exposure to these assets but are niche and less suited for general payments.

- Algorithm: These attempt to maintain their peg through supply-and-demand algorithms, often with no collateral at all. The 2022 collapse of TerraUSD (UST), which erased $40 billion in value, highlighted their fragility. This event led regulators to largely prohibit them and focus instead on fully backed models.

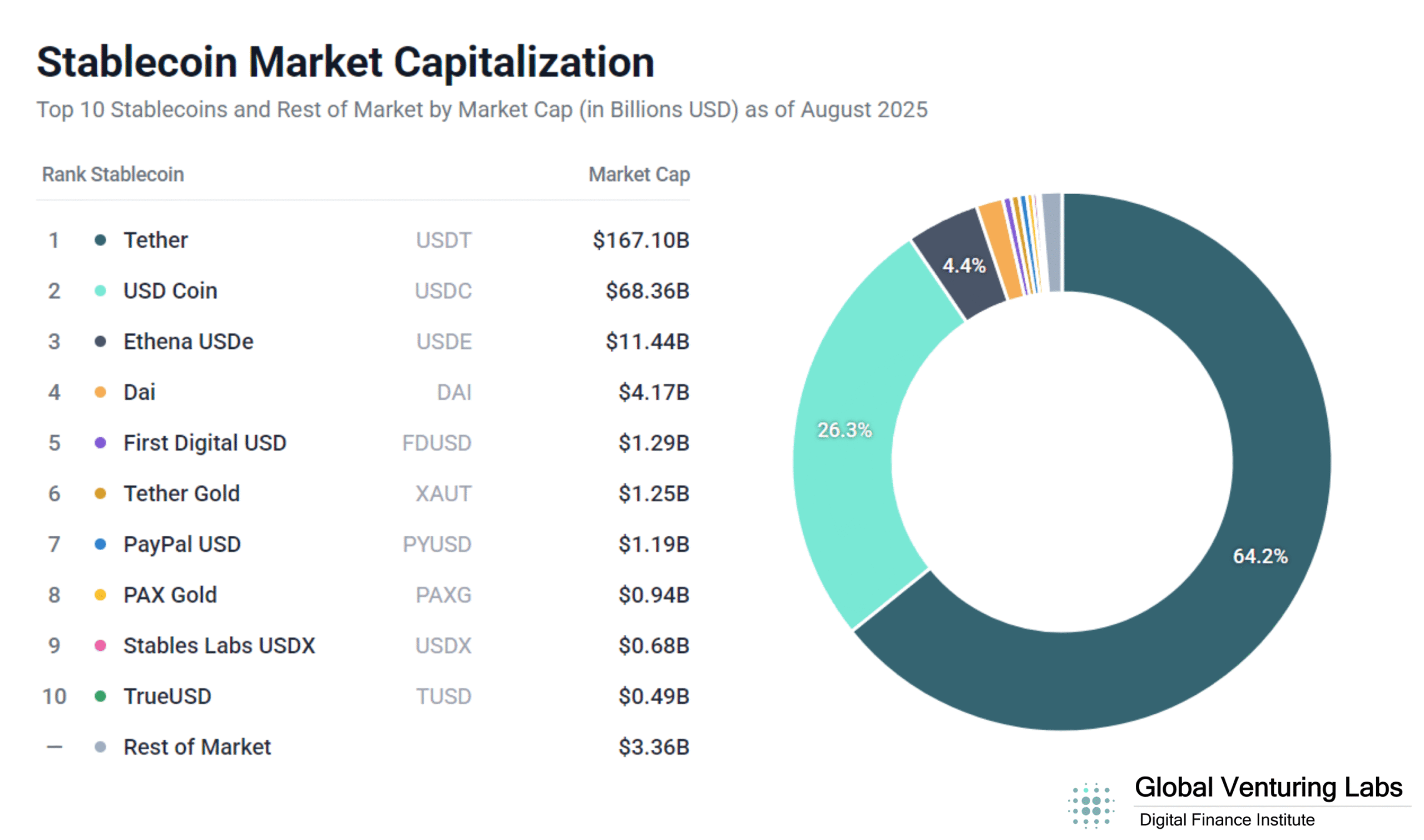

As of August 2025, the stablecoin sector is experiencing significant growth, with annual transaction volumes reaching the trillions of dollars and the number of issued stablecoins now estimated to be well over 220 (Galaxy). This expansion is increasingly driven by traditional financial institutions.

The total market capitalization for stablecoins has swelled to approximately $260 billion, though the market remains highly concentrated (Pantera Capital and Forbes). Tether (USDT) and USD Coin (USDC) continue their dominance, with their combined market caps of roughly $234 billion representing approximately 90% of the entire stablecoin market. The following breakdown highlights this landscape:

Section 3. Regulation

Governments worldwide are rapidly moving to regulate stablecoins, replacing a long period of uncertainty with clear, structured frameworks. This global push is driven by a shared goal: to ensure financial stability and protect consumers by making stablecoin issuers accountable.

The common thread across all major jurisdictions is the focus on asset backing. Regulators are demanding that stablecoins be backed one-to-one by high-quality, liquid assets, such as cash or short-term government bonds, to guarantee that every digital dollar is real. While the goal is the same, the approaches vary slightly:

- The European Union has set a high bar with its comprehensive Markets in Crypto-Assets (MiCA) regulation, which creates a strict licensing regime for issuers.

- The United States is moving toward a pragmatic but restrictive model, aiming to bring stablecoin issuance under the umbrella of federal and state banking regulators.

- Key Asian markets like Japan, Hong Kong, and Singapore have adopted highly restrictive, bank-centric models, ensuring only licensed financial institutions can participate.

The global wave of regulation is creating a safer and more predictable environment. It is this newfound legal clarity that has given traditional financial giants the confidence to finally enter the stablecoin arena.

Section 4. Timeline

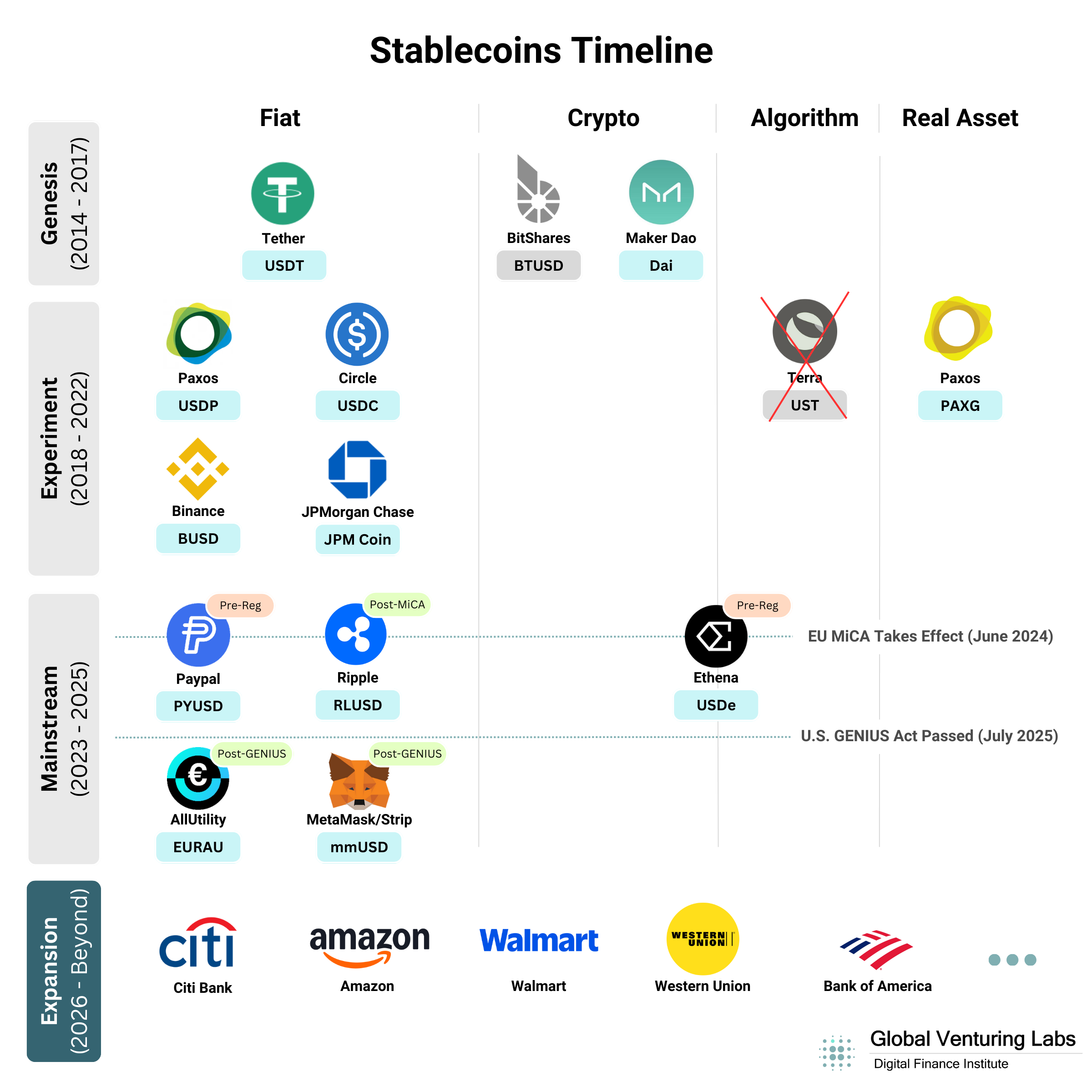

The number and type of stablecoin issuers have increased dramatically since 2014, with the motivation for issuance evolving just as quickly. What began as a tool to solve problems within the crypto ecosystem has become a strategic imperative for the world’s largest financial companies. This evolution can be understood in three distinct eras, each defined by who was issuing stablecoins and why.

1. The Genesis Era (2014-2017): Solving Crypto’s Native Problems

The first stablecoins emerged in 2014 to address problems within the crypto ecosystem, where traders needed a stable asset to transact without constantly converting back into traditional fiat currency. BitShares pioneered the first crypto-collateralized stablecoin (BITUSD), while Tether (USDT) introduced the fiat-backed model that soon became a critical liquidity bridge for exchanges. Later, MakerDAO (DAI) built upon the decentralized approach with an over-collateralized crypto-backed design.

2. The Experiment Era (2018-2022): Refining Models and Testing Boundaries

As the crypto market grew, a new wave of issuers entered to refine existing models and experiment with new ones. Regulated financial institutions like Paxos (USDP) and Circle (USDC) launched compliant, audited stablecoins to attract institutional capital, with Paxos even tokenizing real-world assets like gold (PAXG). At the same time, major banks like JPMorgan Chase built private stablecoins (JPM Coin) for internal settlements.

The motivations became more diverse and business-focused, shifting to goals like monetizing trust, improving corporate efficiency, and controlling a platform’s ecosystem, as seen with Binance’s BUSD. This era’s ambitious search for new models also led to the rise and catastrophic fall of the algorithmic stablecoin Terra (UST), which served as a stark warning about risk and marked a pivotal end to the period of unchecked experimentation.

3. The Mainstream Era (2023-2025): The Great Institutional Entry

The current era is defined by the entry of major, non-crypto-native institutions, catalyzed by newfound regulatory clarity. This is no longer about solving crypto’s internal problems; it’s about building the future of finance. Global payment giants like PayPal (PYUSD) and enterprise solution providers like Ripple (RLUSD) have launched their own stablecoins. New ventures like AllUnity (EURAU) are being formed to specifically target the regulated European market, while wallet providers like MetaMask (mmUSD) are embedding stablecoins directly into their products. This era also features new forms of crypto-native innovation, such as the “synthetic dollar” model of Ethena Labs (USDe), which operates alongside the institutional push.

4. The Expansion Era (2026-Beyond): The Rise of Global Adoption

Beyond the stablecoins already in circulation, a deep pipeline of projects signals that the mainstream era is just beginning. U.S. banking giants like Bank of America and Citigroup are actively exploring their own USD-backed stablecoins for treasury and settlement. This trend is global, with remittance giants like Western Union and tech behemoths like Amazon and Walmart also exploring stablecoins for their vast consumer ecosystems. This pipeline confirms that the world’s leading companies are no longer just observing; they are actively building the future of regulated digital currency.

Section 5. Rationales

The decision by the world’s leading financial and technology institutions to issue their own stablecoins is not driven by a single motive but by a powerful and interconnected set of strategic imperatives. These rationales extend far beyond creating a better payment method; they encompass new revenue models, defensive ecosystem strategies, and a foundational play for the future of a tokenized economy. We can understand these drivers through three core motivations that often overlap and reinforce one another.

Revenue

A core business model for stablecoin issuers is to earn interest revenue from their reserves. The issuer accepts a dollar from a user and gives them a zero-interest stablecoin, then invests that dollar in safe, interest-bearing assets like U.S. Treasury bills. The profit is the yield earned on those reserves.

- USDT, USDC, & USDP: These fiat-backed stablecoins from Tether, Circle, and Paxos generate billions in revenue by earning interest on their massive reserve funds.

- PAXG: Paxos charges fees for the creation, redemption, and on-chain transfer of its gold-backed token.

- DAI: The MakerDAO protocol earns revenue from the “stability fees” (interest) that users pay to borrow DAI against their collateral.

- USDe: The Ethena Labs protocol is designed to capture high yield from its synthetic dollar strategy.

Ecosystem

For large technology platforms with millions of users, issuing a native stablecoin is a classic strategy to build a powerful competitive moat. By creating a proprietary “platform currency,” a company can reduce reliance on external partners, simplify the user experience, and control the primary monetary rail on its platform.

- PYUSD & mmUSD: PayPal and MetaMask launched their stablecoins to make their platforms “stickier,” creating seamless, native payment experiences to increase user engagement.

- BUSD & UST: Historically, this was the goal of Binance’s BUSD on its exchange and Terra’s UST for its blockchain ecosystem.

- BTUSD: One of the earliest examples, this was created as a necessary tool to enable efficient trading on the BitShares decentralized exchange.

Efficiency

The most immediate driver is the profound inefficiency of legacy financial infrastructure like SWIFT and ACH. Stablecoins offer a solution: 24/7/365, near-instantaneous, and low-cost settlement. This is the primary motivation for global banks and enterprise networks looking to upgrade their core services.

- JPM Coin: JPMorgan Chase’s token was created to improve the efficiency and speed of its internal and wholesale payment operations.

- RLUSD: Ripple created its stablecoin to make its core enterprise payment network more efficient for institutional clients.

- EURAU: This stablecoin from AllUnity is a strategic investment to efficiently capture the newly regulated European market under the MiCA framework.

Section 6. Risks

While the push for institutional stablecoins promises greater efficiency, it also creates significant risks. Instead of a unified system, we could see a fragmented landscape, leading to three critical challenges: a lack of interoperability, new threats to financial stability, and a challenge to national economies.

The Interoperability Gap

The biggest risk is creating a chaotic patchwork of digital silos. If every major bank and tech company issues its own proprietary stablecoin, they won’t be easily exchangeable. This would be like the 19th-century “Wildcat Banking” era, where hundreds of banks issued their own private money.

- The Problem: A user couldn’t easily combine “JPM Dollars” with “Citi Dollars.” Merchants would have to accept dozens of different tokens, creating friction and fees for everyone.

- The Result: This outcome defeats the purpose of blockchain technology, which is meant to create seamless, open networks.

Systemic and Contagion Risk

As stablecoins become more integrated into the financial system, they create new pathways for a crisis. The stability of a token depends entirely on the issuer’s ability to honor redemptions.

- The “Bank Run” Scenario: A loss of confidence in a major stablecoin could trigger a digital bank run, forcing the issuer to rapidly sell its reserve assets (like U.S. Treasury bills) to meet redemptions.

- The Spillover Effect: Because major issuers hold vast amounts of government debt, a fire sale of these assets could disrupt critical financial markets, allowing a crisis in the digital world to spill over into the traditional economy.

The Challenge to Monetary Sovereignty

The widespread use of U.S. dollar-pegged stablecoins in other countries, a trend known as “digital dollarization,” poses a threat to national economies.

- The Impact: When a foreign digital currency begins to replace a local one, it limits the ability of that nation’s central bank to manage its own economy through monetary policy.

- The Response: Regulators, particularly in the European Union, are already planning to restrict the use of non-euro stablecoins to protect their financial stability.

Section 7. Oppotunites

The emergence of a regulated, institution-led stablecoin ecosystem creates a wealth of new commercial opportunities. For savvy entrepreneurs, investors, and established firms, this transition represents a greenfield moment to build the foundational companies for the next generation of finance. The opportunities can be understood in four key layers: core issuance, ancillary services, essential infrastructure, and new applications.

Infrastructure and Interoperability Solutions

As highlighted in Section 6, the risk of market fragmentation is the ecosystem’s greatest challenge. Consequently, building the “plumbing” to connect disparate stablecoins is one of the most valuable opportunities. This includes:

- Cross-Stablecoin Bridges: Secure and efficient protocols that allow users to seamlessly exchange one institutional stablecoin for another.

- Universal Wallets & Gateways: Software that lets a merchant accept a “Citi Dollar” or a “JPMD” without needing to know the difference, handling the conversion seamlessly in the background.

The company that creates the “TCP/IP for stablecoins”—a universal standard that makes all regulated stablecoins feel interchangeable—will become an indispensable piece of core financial infrastructure and capture immense value.

Application Layer Innovation

The most significant long-term value will be created at the application layer. With a foundation of trusted and liquid stablecoins, entrepreneurs can build a new generation of financial products and services, including:

- Real-World Asset (RWA) Tokenization: Marketplaces for issuing and trading tokenized securities, real estate, and private credit, using stablecoins as the native settlement currency.

- Institutional DeFi: Decentralized finance protocols with the compliance features necessary to attract capital from traditional financial institutions.

- Programmable B2B Payments: Platforms that leverage stablecoins to automate complex payment workflows in sectors like logistics, trade finance, and insurance.

Section 8. Not the End

The institutional entry into the stablecoin market represents the beginning of a fundamental re-architecting of global finance. This analysis began by asking three critical questions. The answers, drawn from the preceding analysis, provide a clear vision for the future of digital money.

1. Why are the biggest names in finance and tech all racing to issue their own unique digital dollars?

Institutions are driven by a powerful combination of strategic goals that go far beyond simply creating a better payment method. The primary motivations are capturing new revenue streams by earning interest on reserves, building a competitive “ecosystem moat” to lock in users, and gaining an efficiency edge by upgrading slow, outdated financial infrastructure. These rationales reinforce one another, creating a powerful business model that is too valuable to outsource.

3. Could a flood of competing “branded dollars” create a more fragmented and risky financial landscape?

Yes, this is the most significant risk. Without a focus on interoperability, the proliferation of dozens of distinct stablecoins could lead to a “Wildcat Banking 2.0” scenario, creating a chaotic patchwork of digital silos that adds friction and fees. Furthermore, it introduces new vectors for systemic risk, where a crisis in a major stablecoin could spill over into traditional financial markets. Finally, it presents a challenge to the monetary sovereignty of nations through the trend of “digital dollarization.”

3. What will the future of money look like: a single dominant dollar, or a network of many that are seamlessly connected?

The future will not be a single, universal digital dollar but a competitive multitude of them. The critical question is not how many stablecoins exist, but how interoperable they will be. The greatest challenge—and the most significant commercial opportunity—lies in building the universal bridges, wallets, and standards that will allow them all to communicate seamlessly. The goal is not one coin to rule them all, but a network that creates a truly unified and efficient global financial system.

We are now at a crossroads, witnessing what may be the most significant transformation of the monetary system since the end of the Bretton Woods agreement in 1971. The choices made today will define the future of money itself. Are you ready?

Disclaimer: This analysis is based on publicly available information. The information provided is for educational and informational purposes only and should not be construed as financial, legal, or investment advice.

Yifeng Tian

About Global Venturing Labs (GVL)

We warmly welcome you to join our collaborative tech-driven venturing ecosystem.

GVL is a tech-driven venturing platform that empowers innovators by harnessing next-generation technologies, with primary focus on RWA tokenization, to fund innovative ideas and drive wealth creation. GVL fosters an ecosystem where founders, investors, tech experts, and visionaries collaborate seamlessly, transforming concepts into reality in a new era of decentralized venture creation.

Mission and Pillars

- Co-Knowledge Base – Delivering actionable insights, tools, and real-world examples to guide innovators in building thriving ventures. We empower our partners to share their expertise, fostering collective growth and innovation.

- Co-Community Networks – Fostering a global network of visionaries-founders, tech experts, investors, and enthusiasts – to connect, collaborate, and drive innovation.

- Co-Venture Platform – A future decentralized, DAO-based platform empowering members to launch businesses and invest through community-driven funding. We aim to provide values beyond capital.

Join us for the next-gen collaborative venturing!